The higher the deposit, the lower your monthlies will be as you'll have a smaller amount to pay to GFV. You'll pay a little less interest as a result asyour balance throughout the PCP will be lower.That’s why I can’t work it out as if I put in a high deposit I still pay the same amount and the ballon payment is the same. I thought higher deposit would mean the amount I’m borrowing would be less as the ballon payment stays the same

PCP and ownership

- Thread starter Statiker

- Start date

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

APR on pcp deals are fixed for the 4 year term so your balloon will also stay they same alsoI’ve just noticed that the ballon payment with my bank and also with Audi pcp is now the same at around £21k but it’s used to be £17k with my bank. So is the amount you pay over 4 years not a fixed amount? It’s just due to interest? So as the interest rate goes up, you just pay less capital off? I assumed it was a fixed amount say £25k over 4 years and you just pay more on top if rates change?

Oh no I meant is the 4 year term for a certain £ amount? As the higher the Apr the gfv seems to go up. Or is it done on a percentage of the gfv? As my bank pcp used to be say 7.4% and the gfv was around £17k but now it’s 8.9% and gfv around £21/22k so I wondered how it’s all calculatedAPR on pcp deals are fixed for the 4 year term so your balloon will also stay they same also

Have you changed the mileage as that will play a big part in the GFVOh no I meant is the 4 year term for a certain £ amount? As the higher the Apr the gfv seems to go up. Or is it done on a percentage of the gfv? As my bank pcp used to be say 7.4% and the gfv was around £17k but now it’s 8.9% and gfv around £21/22k so I wondered how it’s all calculate

The GFV will be for a certain amount at any given time. It is the bare minimum worth for the car at the given time e.g. a GFV for 3 years PCP duration will be higher than that for a 4 year PCP because a 3 year old car will always be worth more than a 4 year old car.Oh no I meant is the 4 year term for a certain £ amount? As the higher the Apr the gfv seems to go up. Or is it done on a percentage of the gfv? As my bank pcp used to be say 7.4% and the gfv was around £17k but now it’s 8.9% and gfv around £21/22k so I wondered how it’s all calculated

Audi will know what they think a 3 or 4 year old example should p/x at to allow them to make a decent margin reselling it at a price the market will bear.

If they jack the APR rate up without increasing the GFV, the consumer pays more and they get more profit from the finance. If they jack up the APR rate and increase the GFV, they get more, but your monthlies won't necessarily increase because you have less capital to pay back to get to that GFV across your PCP term.

No I always keep it at 10k, maybe it’s just the value is changing as cars are holding more value?Have you changed the mileage as that will play a big part in the GFV

Yes, Audi think the used market will bear the higher used prices, so GFV going up cancels out the higher APR% - more interest to pay, but less capital to pay off - keeps the monthlies about the same.No I always keep it at 10k, maybe it’s just the value is changing as cars are holding more value?

Last edited:

I've signed an agreement for my S3 this afternoon at 10.7%. I'm picking up the car on Friday. I could get a recalculation to get the lower rate, but as the £3k deposit contribution is the same and I'll be paying off the balance a day or 2 after collection, it's not a bother.They’ve also dropped the Apr from 10.6 to 9.8%. For some reason an a4 is only 6%, guess they are trying to sell more a4’s

I'd still be asking the question to why you haven't got the lower APR as it is defiantly 9.9% nowI've signed an agreement for my S3 this afternoon at 10.7%. I'm picking up the car on Friday. I could get a recalculation to get the lower rate, but as the £3k deposit contribution is the same and I'll be paying off the balance a day or 2 after collection, it's not a bother.

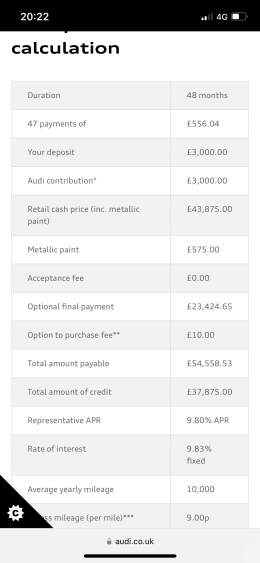

Oh one more thing, why is the total amount payable for an S3 going to be £54k when it’s only borrowing about £26k over the 4 years? A loan for 26k for 4 years at the same Apr is about £5k interest where as my calculation is over £10k interest on this pcp. I know the £54k includes the balloon payment at the end but is all that interest just for the circa £26k over the 4 years? Or am I missing something?

Attachments

I arranged finance around a month ago when I first placed the order on a car that was built and on its way, with the old terms in place from then. If I wasn't settling up immediately, I'd be asking that question. As it is, if this costs me 40p in interest before I exercise my right to withdraw, I won't lose any sleep over it.I'd still be asking the question to why you haven't got the lower APR as it is defiantly 9.9% now

You are missing something. You are borrowing the whole car cost (£43k), but deferring paying off the GFV amount. On month 1 you are paying interest on the whole whack. On month 48 you are still paying interest on the GFV amount, so you are paying about twice the interest you think you are.Oh one more thing, why is the total amount payable for an S3 going to be £54k when it’s only borrowing about £26k over the 4 years? A loan for 26k for 4 years at the same Apr is about £5k interest where as my calculation is over £10k interest on this pcp. I know the £54k includes the balloon payment at the end but is all that interest just for the circa £26k over the 4 years? Or am I missing something?

In year 1, with a tiny deposit down, you'd be paying around £300 a month in PCP interest alone and at the end of the term about £130pm of your monthly payment will be PCP interest.

PCP and deferred GFV means you will always be paying interest on a large chunk of the car vost and you are paying off capital slower than you probably think you are.

Ah yeah course I forgot about that! So I should be comparing it to a loan for £43k reallyYou are missing something. You are borrowing the whole car cost (£43k), but deferring paying off the GFV amount. On month 1 you are paying interest on the whole whack. On month 48 you are still paying interest on the GFV amount, so you are paying about twice the interest you think you are.

In year 1, with a tiny deposit down, you'd be paying around £300 a month in PCP interest alone and at the end of the term about £130pm of your monthly payment will be PCP interest.

PCP and deferred GFV means you will always be paying interest on a large chunk of the car vost and you are paying off capital slower than you probably think you are.

Compare it with a £43k loan over 6 years that you cash out of after 3 years,by selling your 3 year old car to pay off the remaining 3 years of the loan (or sell your 4 year old car to pay off the remaining 2 years). When the interest rate is so high, you might want to check out the difference between a 3 year PCP term and a 4 year PCP term - the monthly difference might be surprisingly small.Ah yeah course I forgot about that! So I should be comparing it to a loan for £43k really

fair enoughI arranged finance around a month ago when I first placed the order on a car that was built and on its way, with the old terms in place from then. If I wasn't settling up immediately, I'd be asking that question. As it is, if this costs me 40p in interest before I exercise my right to withdraw, I won't lose any sleep over it.

So where it says “total amount of credit “this is the amount of credit I’ll be paying interest on but not how much I’ll be paying off over the term isn’t it? If I give the car back after the 4 years (48x £565 payments) I’m just paying £27000 to have used the car for 4 years? If the car has a gfv of £24k and the car is worth say £28k, Audi would give me £4k towards another pcp deal?Compare it with a £43k loan over 6 years that you cash out of after 3 years,by selling your 3 year old car to pay off the remaining 3 years of the loan (or sell your 4 year old car to pay off the remaining 2 years). When the interest rate is so high, you might want to check out the difference between a 3 year PCP term and a 4 year PCP term - the monthly difference might be surprisingly small.

In fact it would be £30k to use the car for 4 years as there was also £3k deposit. That’s a lot just to use a car for 4 years isn’t it?I’ve just noticed that the ballon payment with my bank and also with Audi pcp is now the same at around £21k but it’s used to be £17k with my bank. So is the amount you pay over 4 years not a fixed amount? It’s just due to interest? So as the interest rate goes up, you just pay less capital off? I assumed it was a fixed amount say £25k over 4 years and you just pay more on top if rates change?

Basically you're pretty much paying the depreciation of the car over the 4 year term plus interest .In fact it would be £30k to use the car for 4 years as there was also £3k deposit. That’s a lot just to use a car for 4 years isn’t it?

On a £43k car with a GFV of £24k after 4 years, and a deposit contribution, you'll have paid off £16k capital (plus £3k capital from the deposit contribution) and approx £11k interest over 48 x £565 payments.So where it says “total amount of credit “this is the amount of credit I’ll be paying interest on but not how much I’ll be paying off over the term isn’t it? If I give the car back after the 4 years (48x £565 payments) I’m just paying £27000 to have used the car for 4 years? If the car has a gfv of £24k and the car is worth say £28k, Audi would give me £4k towards another pcp deal?

With an interest rate sohigh, have you considered whether the 3 year monthlies are significantly more expensive than the 4 year monthlies? I bet there's very little in it.

£11k interestOn a £43k car with a GFV of £24k after 4 years, and a deposit contribution, you'll have paid off £16k capital (plus £3k capital from the deposit contribution) and approx £11k interest over 48 x £565 payments.

With an interest rate sohigh, have you considered whether the 3 year monthlies are significantly more expensive than the 4 year monthlies? I bet there's very little in it.

this is why I put in as much as possible deposit and over pay where I can to get the car paid off by asap .

this is why I put in as much as possible deposit and over pay where I can to get the car paid off by asap .I've had my car paid off for 18 months and i'am really apprehensive to get into another agreement with the APR's so high .

£11k interest

I've had my car paid off for 18 months and i'am really apprehensive to get into another agreement with the APR's so high .

I picked up my S3 last night and I'll be withdrawing from the agreement on Monday. £44.5k inc. service plan and warranty extension, £1700 discount, £3k deposit contribution, £10k down, £29.8k to settle. If you've got the cash or finance arranged elsewhere, that deposit contribution is free money.

Totally agree . Congrats have you put any pics of the of S3 on here yetI picked up my S3 last night and I'll be withdrawing from the agreement on Monday. £44.5k inc. service plan and warranty extension, £1700 discount, £3k deposit contribution, £10k down, £29.8k to settle. If you've got the cash or finance arranged elsewhere, that deposit contribution is free money.

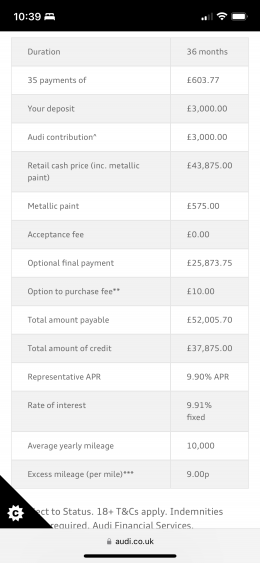

It’s £38 more a month for 36 months. So that’s around £21k instead of £26k in payments? But gfv is obviously higherOn a £43k car with a GFV of £24k after 4 years, and a deposit contribution, you'll have paid off £16k capital (plus £3k capital from the deposit contribution) and approx £11k interest over 48 x £565 payments.

With an interest rate sohigh, have you considered whether the 3 year monthlies are significantly more expensive than the 4 year monthlies? I bet there's very little in it.

Attachments

£38 more a month. For that £1296 extra paid, you save a year's VED (about £530), and will have a warranty throughout, vs having no warranty in year 4 unless you buy it for about £300. Up to you whether you think its worth it.It’s £38 more a month for 36 months. So that’s around £21k instead of £26k in payments? But gfv is obviously higher

I'am guessing this is direct through Audi if soIt’s £38 more a month for 36 months. So that’s around £21k instead of £26k in payments? But gfv is obviously higher

Wouldn't you be better off ordering through DTD or coast2coast for a better deal

Looks like current discount on an S3 is running at about £4900 including the £3k deposit contribution on drivethedeal. If I was ordering from scratch, I would order from there - always cheaper than Carwow, and probably cheaper than coast2coast cars (who were always best for BMW deals).I'am guessing this is direct through Audi if so

Wouldn't you be better off ordering through DTD or coast2coast for a better deal

My salesmanat pickup said Audi are moving to the direct ordering approach soon. Your local dealership will be servicing, window shopping and collection only. No haggling, no deals, just what tge website says you'll pay.

How do you work out the extra capital paid on pcp vs interest?£38 more a month. For that £1296 extra paid, you save a year's VED (about £530), and will have a warranty throughout, vs having no warranty in year 4 unless you buy it for about £300. Up to you whether you think its worth it.

Take the list price of the car, takeaway any discounts or incentives. This is the real price of the car to you.How do you work out the extra capital paid on pcp vs interest?

Take that value and knock off the GFV - the difference is how much capital you're clearing.

Calculate how much you're paying over the term by adding any deposit you're paying to the monthlies x number of months.

E.g. Let's say you're buying a £43k car that comes with £3k deposit contribution and £1500 discount. Let's also say you put down £5k deposit and it has a 3 year GFV of £27k,with monthlies of £550.

£43k - £3k - £1.5k = £38.5k real cost excluding interest, if you buy it.

£38.5k - £27k GFV = £11.5K capital cleared in PCP term.

Total paid in PCP term = £5k + (35 x £550) = £24.25k

Total interest paid = £24.25 - £11.5k = £12.75k.

Half of what you're paying out over the PCP term is interest with these crazy 10% APRs.

I just rang VWFS as I was pleasantly surprised that they are open on a Saturday morning. Went through the automated route, not speaking to a human and could only pick "settlement" - figure of £30239.57 came up. This isn't right, my agreement had £29734.76 being financed.Totally agree . Congrats have you put any pics of the of S3 on here yet

Found a way through the menu paths to speak to a human and he could see my "settlement figure" - it includes a standard 58 days of interest added in. The automated calculation isn't clever enough to recognise you've only had the car a day and are within the "withdrawal period". My withdrawal price is "£29751.52", including 2 days interest of about £8.50 a day. That's yesterday and today. Thought it was a bit cheeky to charge 2 days interest when I'd had the car 20 hours!

I don't think that will work out well for themLooks like current discount on an S3 is running at about £4900 including the £3k deposit contribution on drivethedeal. If I was ordering from scratch, I would order from there - always cheaper than Carwow, and probably cheaper than coast2coast cars (who were always best for BMW deals).

My salesmanat pickup said Audi are moving to the direct ordering approach soon. Your local dealership will be servicing, window shopping and collection only. No haggling, no deals, just what tge website says you'll pay.

they have had to drop the APR twice through lack of sales offering no discount

would further dampen sales imo

I don't either, they must think there's cost savings to be made doing it that way.I don't think that will work out well for them

they have had to drop the APR twice through lack of sales offering no discount

would further dampen sales imo

I was politely asked to give them a great survey review - if you don't give them 5* Audi penalises them apparently. The salesman said he lot £400 in his pay packet because one 4* collection survey rating (with no negative comments) had dropped him below 98.5% satisfaction rating.

I will give top marks, as he was really proactive in chasing up bits for me, and if you hurt their bottom line, they won't have access to Audi bonuses that allow then to give you a discount.

My handover from Canterbury was a bit rubbish, salesman I had dealt with all the way through and up to the day before didn't mention he wouldn't be in so had to hang around for someone else to do it, he also forgot to mention I had to pay £1k deposit as I had a private reg, then the WiFi wouldn't work when they were registering everything...oh yeah we know its terrible in here, then it took 3 months and many calls to get my £1k back after being told I would get it back immediately after they received my docsI don't either, they must think there's cost savings to be made doing it that way.

I was politely asked to give them a great survey review - if you don't give them 5* Audi penalises them apparently. The salesman said he lot £400 in his pay packet because one 4* collection survey rating (with no negative comments) had dropped him below 98.5% satisfaction rating.

I will give top marks, as he was really proactive in chasing up bits for me, and if you hurt their bottom line, they won't have access to Audi bonuses that allow then to give you a discount.

My handover from Canterbury was a bit rubbish, salesman I had dealt with all the way through and up to the day before didn't mention he wouldn't be in so had to hang around for someone else to do it, he also forgot to mention I had to pay £1k deposit as I had a private reg, then the WiFi wouldn't work when they were registering everything...oh yeah we know its terrible in here, then it took 3 months and many calls to get my £1k back after being told I would get it back immediately after they received my docs

Mine's been fine so far. He popped the bonnet to show me the engine bay and I noticed that the terminal flap/cover on the minus terminal of the 12V battery was missing - he's ordered me a new one. The 4 rings puddle lights weren't fitted, but the box was there in teh glovebox. He offered to fit there and then, but as I had a drive back to Newcastle from Grimsby, I declined. I'll be fitting dual dashcans as soon as my new 3M stocky pads arrive from Ebay, so i'm sure I can manage to fit a few puddle lights. Tempted to fit them in the back and get some S3 ones for the fronts from Aliexpress or similar.

Would ideally like to get some DSG paddle extensions also.

Nice pics btw ...I'll be looking out for it as not too far away from youMine's been fine so far. He popped the bonnet to show me the engine bay and I noticed that the terminal flap/cover on the minus terminal of the 12V battery was missing - he's ordered me a new one. The 4 rings puddle lights weren't fitted, but the box was there in teh glovebox. He offered to fit there and then, but as I had a drive back to Newcastle from Grimsby, I declined. I'll be fitting dual dashcans as soon as my new 3M stocky pads arrive from Ebay, so i'm sure I can manage to fit a few puddle lights. Tempted to fit them in the back and get some S3 ones for the fronts from Aliexpress or similar.

Would ideally like to get some DSG paddle extensions also.

It’s a known issue on here. You do not get the covers on the battery terminal. The consensus being that it is a cost saving.Mine's been fine so far. He popped the bonnet to show me the engine bay and I noticed that the terminal flap/cover on the minus terminal of the 12V battery was missing - he's ordered me a new one. The 4 rings puddle lights weren't fitted, but the box was there in teh glovebox. He offered to fit there and then, but as I had a drive back to Newcastle from Grimsby, I declined. I'll be fitting dual dashcans as soon as my new 3M stocky pads arrive from Ebay, so i'm sure I can manage to fit a few puddle lights. Tempted to fit them in the back and get some S3 ones for the fronts from Aliexpress or similar.

Would ideally like to get some DSG paddle extensions also.

I had no idea that it would be a cost saving thing, surely the terminal covers come with the battery and they pull them off for access, to connect the battery, and should clip them back on afterwards? I can't imagine the terminal covers being extra pieces. It's just a little polythene flap with 2 pegs to fit in to 2 holes on the battery body. There's always one on the positive terminal (as there should be).It’s a known issue on here. You do not get the covers on the battery terminal. The consensus being that it is a cost saving.

Busy day for the car's post.

V5 turned up, as did my 3M sticky pads for re-installing my dashcam, a welcome letter from VWFS, a settlement letter from VWFS and a withdrawal letter from VWFS, as well as that 12V battery negative terminal cover/flap.

V5 turned up, as did my 3M sticky pads for re-installing my dashcam, a welcome letter from VWFS, a settlement letter from VWFS and a withdrawal letter from VWFS, as well as that 12V battery negative terminal cover/flap.